The Role of Bookkeepers in Reducing Financial Errors and Business Risks

Financial accuracy is essential for any business that wants to remain stable and competitive. Even small errors in accounting records can lead to serious consequences such as cash flow issues, tax penalties, or poor decision-making. Many business owners focus on growth and operations, but financial management often requires specialized attention. This is where professional bookkeeping services Gold Coast play an important role. They help maintain accurate records, monitor transactions, and reduce the risks associated with financial mistakes. Understanding the role of bookkeepers in reducing financial errors and business risks explains why they are essential for long-term business success.

Maintaining Accurate Financial Records

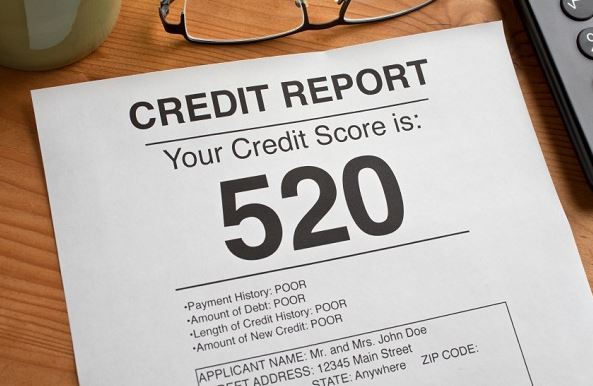

One of the primary responsibilities of bookkeepers is maintaining precise financial records. Every transaction must be recorded correctly to reflect the true financial position of a business. Bookkeepers track income, expenses, invoices, and payments in a structured and organized system. This reduces confusion and ensures that no transaction is overlooked. Accurate records allow businesses to understand their financial health at any given time. Without proper bookkeeping, errors can quickly accumulate and create misleading financial reports. Reliable recordkeeping forms the foundation for all other financial processes, including budgeting and forecasting.

Preventing Data Entry and Calculation Errors

Manual data entry mistakes are one of the most common causes of financial errors in businesses. Even a small typo or miscalculation can affect overall financial reports. Bookkeepers use systematic processes and accounting software to reduce these risks. They carefully review entries to ensure consistency and accuracy across all financial documents. Regular checks …

One of the most popular loans online is the Liberty Loan. This loan offers a low fixed interest rate and allows borrowers to borrow up to $50,000 with no down payment. The repayment terms are flexible and can range from five to fifteen years depending on the amount borrowed. The main benefit of this loan is that it provides borrowers with access to funds quickly and easily, without the need for a credit check.

One of the most popular loans online is the Liberty Loan. This loan offers a low fixed interest rate and allows borrowers to borrow up to $50,000 with no down payment. The repayment terms are flexible and can range from five to fifteen years depending on the amount borrowed. The main benefit of this loan is that it provides borrowers with access to funds quickly and easily, without the need for a credit check.

One of the biggest mistakes business owners can make when seeking financing is not doing enough research ahead of time. You must understand the different types of funding available and the terms and conditions associated with each one. Otherwise, you could end up paying more than you need or signing away equity in your company.

One of the biggest mistakes business owners can make when seeking financing is not doing enough research ahead of time. You must understand the different types of funding available and the terms and conditions associated with each one. Otherwise, you could end up paying more than you need or signing away equity in your company. Another common mistake is not having a well-developed business plan. This document should outline your company’s goals, revenue streams, and expenses. Potential investors will use it to determine whether or not they want to provide funding. If you do not have a strong business plan, it is unlikely that you will be able to secure the financing you need.

Another common mistake is not having a well-developed business plan. This document should outline your company’s goals, revenue streams, and expenses. Potential investors will use it to determine whether or not they want to provide funding. If you do not have a strong business plan, it is unlikely that you will be able to secure the financing you need. It is also important to avoid asking for more money than you need. This can be a red flag for investors, who may wonder why you are not being more frugal with your finances. It is better to ask for less money than you need and then requests more …

It is also important to avoid asking for more money than you need. This can be a red flag for investors, who may wonder why you are not being more frugal with your finances. It is better to ask for less money than you need and then requests more …

A single overlooked accounting figure or guideline can mean the difference between a balanced budget and a long night of cause-finding. A company can be at financial risk if it misses numbers or a decimal point. Accountants must pay attention to detail and work meticulously. Accountants must be able to control their work until it becomes second nature to them.

A single overlooked accounting figure or guideline can mean the difference between a balanced budget and a long night of cause-finding. A company can be at financial risk if it misses numbers or a decimal point. Accountants must pay attention to detail and work meticulously. Accountants must be able to control their work until it becomes second nature to them. Accepting the results and the resulting problems is a good quality for an accountant. Accountants must admit that they have …

Accepting the results and the resulting problems is a good quality for an accountant. Accountants must admit that they have …

to ask security in case you default …

to ask security in case you default …